By: Rick Newman

Original Post: https://finance.yahoo.com/news/people-are-running-out-of-money-213744569.html

One mystery of the labor shortage is the missing paycheck: How long can people choosing not to work last without an income?

Nobody’s sure, but clues are emerging. The economy continues to recover from the COVID wipeout, and hiring remains strong. Yet Americans are beginning to report more difficulty paying routine bills, not less, and it’s probably related to the end of federal relief measures that kept millions above water during the last 20 months.

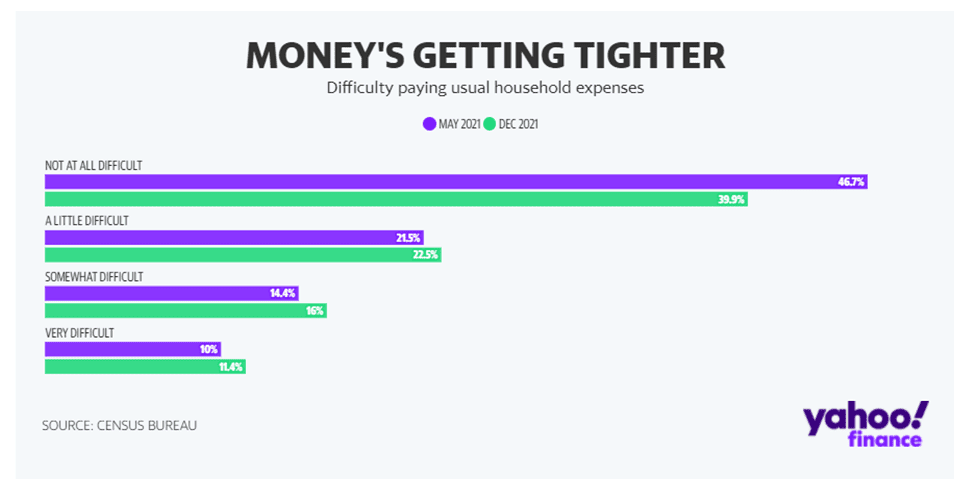

In the Census Bureau’s “household pulse” survey last May, 46.7% of respondents said they had no difficulty paying usual household expenses. By December, that had fallen to 39.9%. During the same time period, the portion saying it’s a little, somewhat or very difficult to pay those bills rose from 45.9% to 49.9%. (The remaining 10% or so did not answer the question.)

Since the economy has been steadily improving, the deterioration in household finances isn’t due to worsening unemployment or falling incomes. But the last stimulus payments went out in the first half of 2021, and emergency federal jobless benefits ended in September. With inflation at 6.8%, buying power is also eroding at the same time aid is drying up.

“There are people who are running out of money,” says Philippa Dunne of TLR Analytics. “It’s getting harder for them to pay their bills. The expiration of expanded unemployment insurance benefits and stimulus payments have taken a toll on household finances.”

There seem to be plenty of jobs for people who need to work. Employers report 10.6 million job openings, nearly the most ever. Unfilled jobs hit unprecedented levels in 2021, as COVID-related anomalies wrought havoc with the labor force. Some parents who want to work must now deal with unpredictable school schedules and an acute shortage of affordable child care. Several million potential workers may still be too concerned about catching COVID on the job to return. Federal aid money has given millions more a financial cushion that could delay a return to work or let them hold out for a better job longer than they may have been able to get before. A record-high quit rate—the portion of workers choosing to leave their jobs—suggests workers have newfound leverage, and they’re using it.

If jobs are there for the taking, people starting to feel a financial pinch should have no trouble nabbing a paycheck or finding new work that pays more or offers better flexibility. But the door to work might not be as wide open as aggregate data suggests. Job-seekers say companies seem to post some listings just to see if they can lure a dream candidate, who never materializes, leaving those jobs open indefinitely. Not all employers are boosting pay and benefits. Some parents can’t find any job offering enough flexibility to let them care for kids or sick family members.

Financial strains could get worse. Another important element of federal relief—an expanded child tax credit—expired in December and it’s not clear Congress will renew it.

The baseline child tax credit remains in place, but the expansion was worth hundreds or thousands of dollars extra to qualifying families. It also allowed those families to claim half the credit in advance, through a monthly bank-account direct deposit or check in the mailbox. The December Census survey showed 39% of child tax credit recipients—nearly 20 million households—spent the money, most likely on necessities. Thirty-eight percent said they used the money to pay down debt and just 26% said they saved it.

One surprise of the COVID pandemic was a broad improvement in household finances, when many economists expected soaring unemployment to make things much worse. Roughly $6 trillion in relief programs passed by Congress gets much of the credit. Consumers also became frenetic savers, since it was hard to spend money when businesses shut down or it felt unsafe to go out. The saving rate rocketed from 8.3% before the pandemic to a high of 33.8% in April 2020. It stayed elevated for the next 15 months, providing a financial cushion as businesses struggled to get back to normal.

That cushion is evaporating. The saving rate in November fell to 6.9%, and Census data shows that more people are now using credit cards to pay for routine expenses. A saving supercycle has now yielded to “dissaving,” when people spend down their surplus and start to borrow more.

None of this means the economy is in particular trouble in 2022, since growth remains solid and robust hiring should resume once the Omicron COVID variant begins to retreat. But tougher economic times for at least some Americans will shape political decisions in 2022 and probably impact the upcoming midterm elections.

There are murmurs in Washington about another round of aid for business and perhaps some consumers still struggling. If it happens, it won’t be nearly as big as last year’s $2 trillion package, but it would reignite disputes between liberal politicians who think Washington should do much more and conservatives who think it has already gone way too far.

Also lingering is President Biden’s “build back better” legislation, which Democrats are revamping in the hope it can pass by the end of February. One of the biggest issues is whether to reauthorize the expanded child tax credit for another year or longer, or revert permanently back to the baseline credit. That bill could also include child care assistance and other measures that might help sidelined workers get back in the action. The question for 2022 is how much help they actually need.

_______________________________________

Rick Newman is a columnist and author of four books, including “Rebounders: How Winners Pivot from Setback to Success.” Follow him on Twitter: @rickjnewman. You can also send confidential tips.