In 2020 and 2021, government spending rose by almost £400 billion, covering policies from furlough to free school meals. This spending dominated the national conversation, but as many of those programs wound down and inflation began to rise, the focus inevitably shifted to taxes.

By: Nikhil Woodruff.

Original post can be found here.

At the Autumn and Spring Budgets of 2021, the Chancellor announced a series of tax raises amounting to around 2% of GDP, mainly from increases to Income Tax and National Insurance. These have had a mixed reception: described simultaneously as progressive and regressive. There is, however, one thing economists might agree on: raising taxes on income will reduce economic growth. For example, the Office for Budget Responsibility estimates that the behavioural response to the NI rise will eliminate 23% of its theoretical revenue.

Taxing labour income reduces labour supply, and this notion applies to many other tax bases, too: profit, property, or even carbon emissions. But one type of thing escapes it, and by doing so has become the favourite among economists: land. In the words of the OECD, “the reviewed evidence and the empirical work suggests recurrent taxes on immovable property being the least distortive tax”.

This raises two questions: what actually is land, and why should we tax it?

Land, defined

These questions were of particular importance to Henry George, the influential American political economist of the 19th century. His most famous work, Progress and Poverty, sought to explain why poverty continues to exist in times of technological advancement, proposing that the answer lies in the rents demanded by owners of natural resources which increase in value. Land, under this definition, encompassess everything not man-made. For property owners, the land you own is the ground underneath your house.

It’s important to distinguish between land area (the physical area covered by a plot of land) and land value (its fair market price). A tax on land refers to the latter, a tax on its value. But where does the value of land come from? Why is an acre of land worth 100 times more in the City of London than in Broxtowe? George posits that this gain comes from the development and productivity surrounding the land, none of which were contributed by the owner. The owner of the land, however, profits when the land value increases. If they are a landlord, they can charge higher rent; if they are their own tenant, they benefit from the improved location value of their residence (and they capture this financially when they sell). According to George, this unearned nature of land values justifies a land value tax, equal to the annual profit of the landowner (the “rent”).

A land dividend in the UK

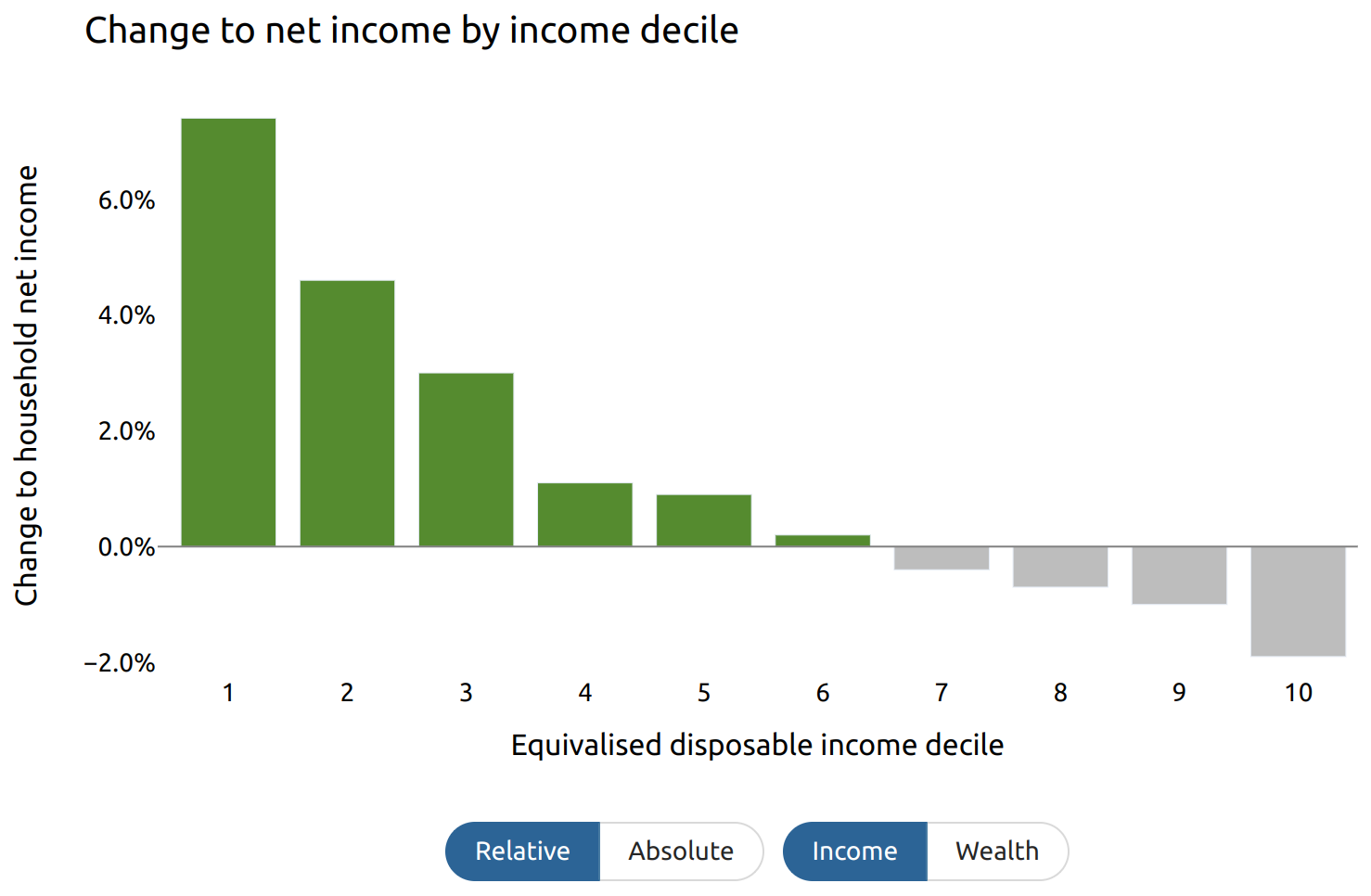

The UK’s total land value exceeds £6 trillion, and thus a land value tax of 1% would raise over £60bn annually. Returning this revenue to UK residents as an £18 per week dividend ensures budget neutrality; this is sometimes called a land dividend. My nonprofit, PolicyEngine, has built an app to compute the impact of tax and benefit reforms such as land dividends. The PolicyEngine app estimates that this 1% land dividend would cut poverty by 18% and benefit two thirds of the population. It would also be highly progressive: the bottom income decile sees its income increase by over 7%, while the upper decile would lose 2%.

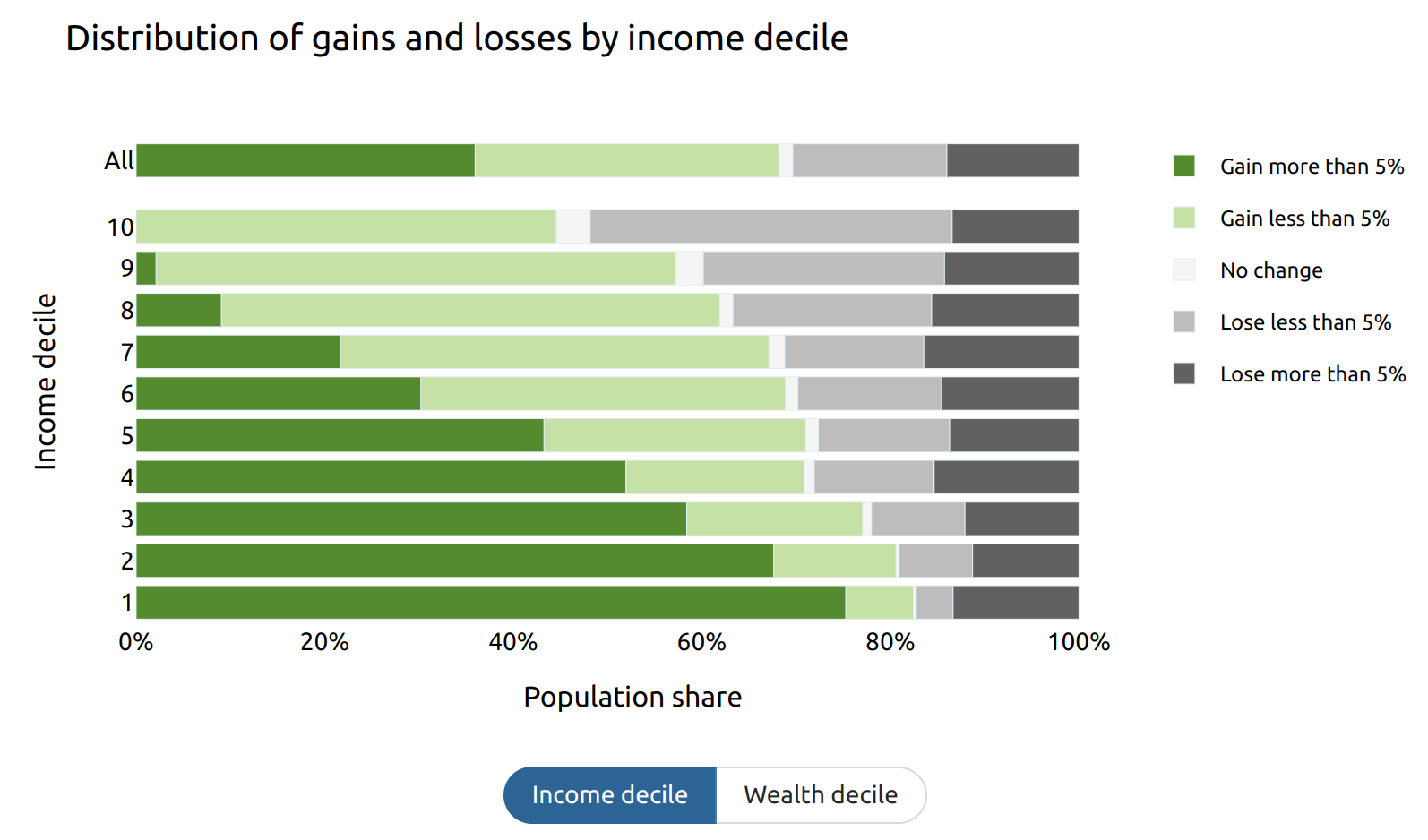

But not everyone comes out ahead, even in the lowest income deciles: at least 17% of every income decile loses more in taxes than they gain from the dividend.

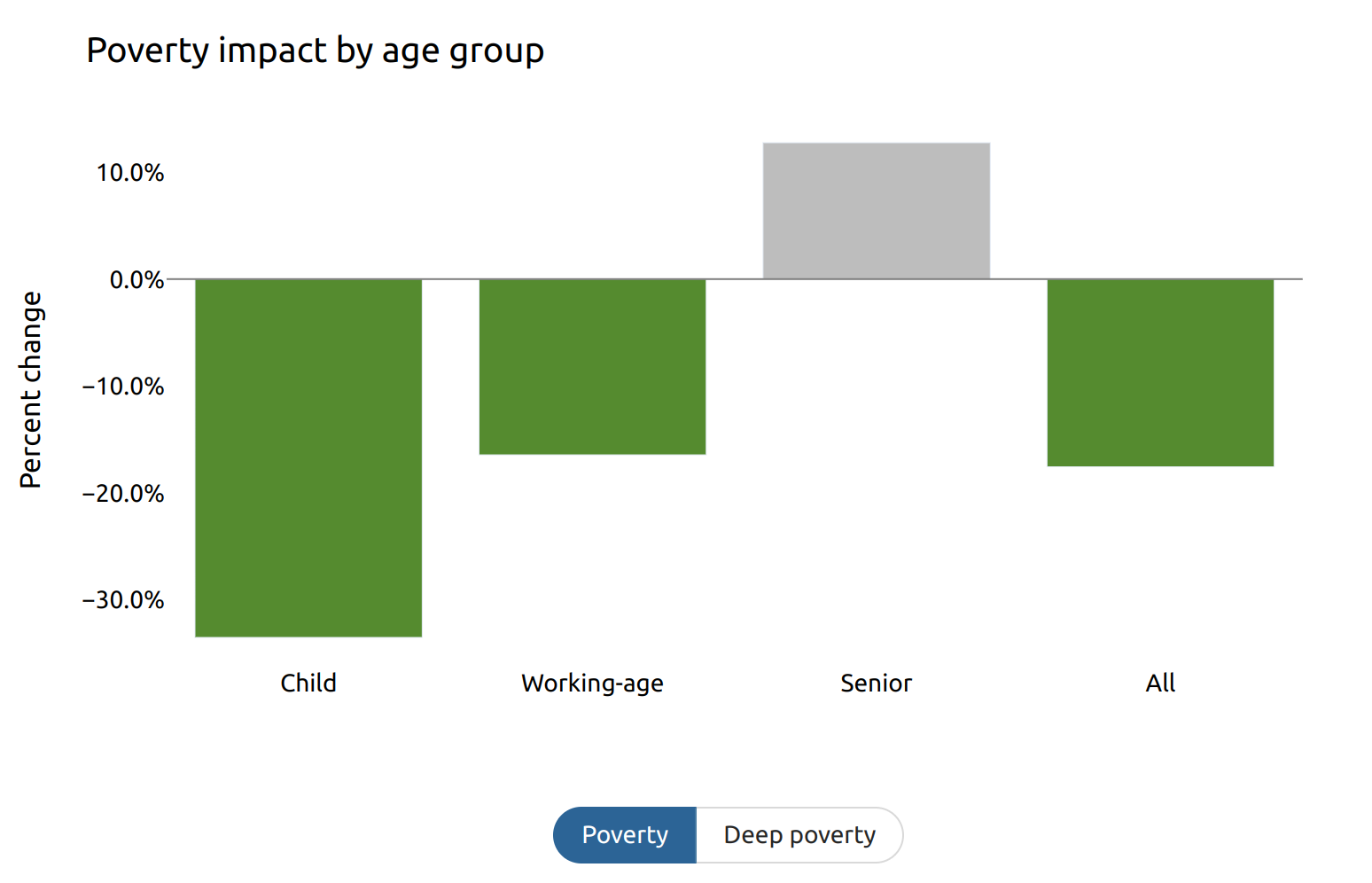

The households who lose out are often senior citizens, many of whom are low-income but asset-rich. Under our estimates, while child poverty falls by 34% and working-age poverty falls by 16%, the poverty rate for pensioners would increase by 13%.

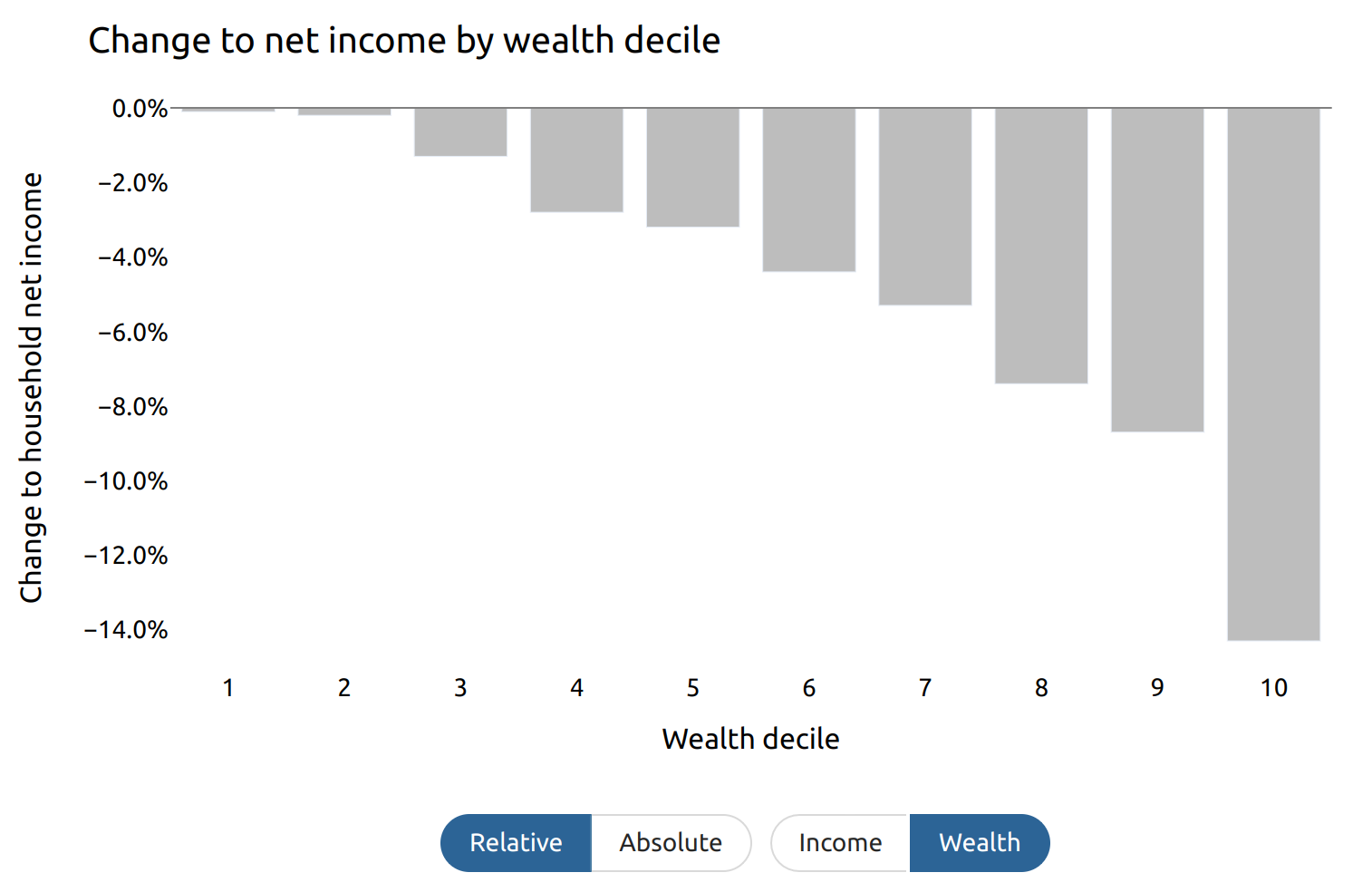

These results present a less-than-perfect outcome: substantial reductions in poverty, but losses among low-income pensioners. But how “progressive” or “regressive” a policy looks depends on how you define “rich” or “poor”. Usually, we order households by their disposable income after taxes and benefits, adjusted for household size: this leads to large percentage losses for low-income (but high-wealth) households, typically comprising retired individuals. But when we order households by their total wealth, we get a different picture, one in which land value taxes are highly progressive:

This applies to the distributions of outcomes within deciles, too: while 17% of the first income decile (and more in higher deciles) lose out from the land dividend, all households in the first three wealth deciles see their net income rise.

There are other issues at play here which the modelling doesn’t answer: how would households and firms change their behaviour in response? Would pensioners in reality avoid poverty by renting out their high-value homes rather than choosing to consume their own housing supply?

Our analysis here is static, only considering immediate effects on the UK by simulating the taxes and benefits each household would pay, before and after (all our modelling is open-source, meaning anyone can see our full working, or tweak our assumptions and parameters). Macroeconomic models might reveal the long-term effects of land value taxes: for example, any positive effects on economic growth by replacing taxes on labour with taxes on land.

These are all important questions, and the evidence base on land taxes will continue to grow, suggesting high revenues and progressive outcomes where that revenue is used effectively. But regardless of the details of that progressivity, land value’s unique properties of a vast, largely untapped source of funds, and the economic efficiency of taxing it, should earn it a far larger share of modern public discourse around taxation.